Friendly Fraud

What is Friendly Fraud?

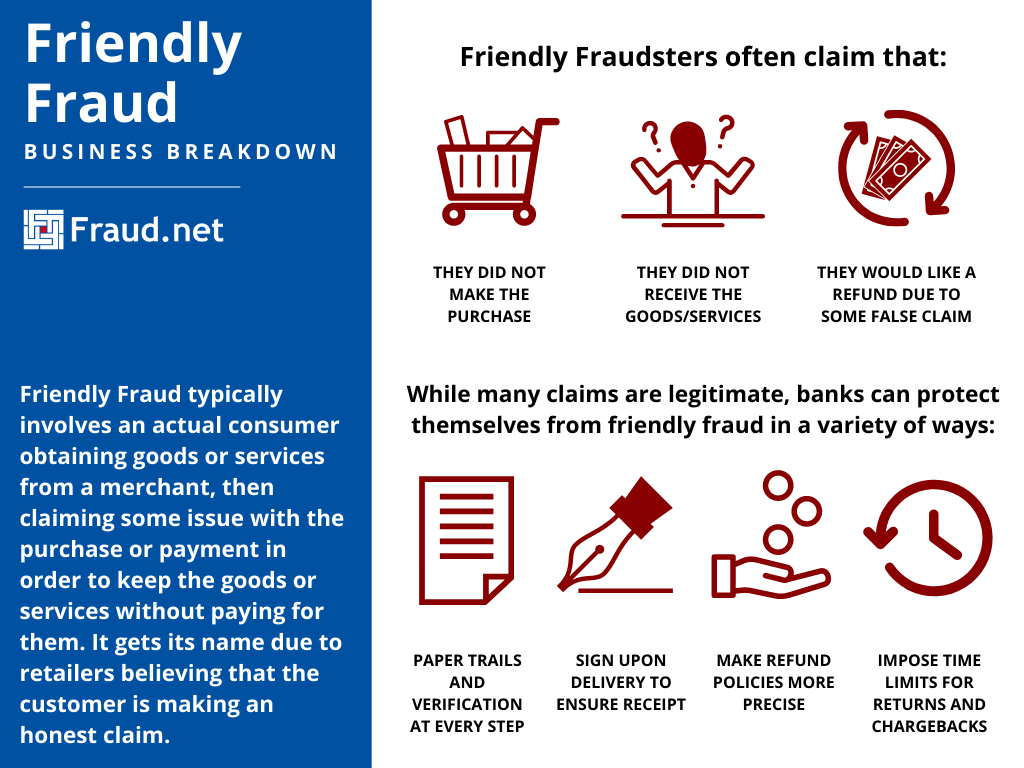

Friendly Fraud, also referred to as first-party fraud, can take many forms, but typically involves an actual consumer obtaining goods or services from a merchant, then claiming they did not make the purchase, did not receive the goods, request a refund from a false claim, or only received a fraction of items, in order to keep the goods or services without paying for them. It gets its name due to retailers believing that the customer is making an honest claim. “Friendly fraudsters” are often good at their crimes, which can sometimes make it hard for customer service to point out a fraudulent claim.

Customers committing friendly fraud make the purchase on a credit card, receive the product or service, and then demand a refund for a lost or short-shipped order, or file a chargeback through their credit card issuing bank, with the intention of receiving a full refund of the purchase amount. Also referred to as chargeback fraud, it is estimated that $4.8 billion was lost by US businesses last year to friendly/chargeback fraud. It is also estimated that as much as 80% of all chargebacks are fraudulent.

How Do You Identify Friendly Fraud?

Identifying friend fraud can be very difficult because of the customer claims that seem believable. Businesses can eliminate the amount of friendly fraud from occurring through tracking and shipping procedures. This could entail that the customer must sign upon delivery, or the business can implement paper trails to prove product orders and delivery. Clear and precise refund policies can also reduce customer fraud claims on falsified product descriptions. Lastly, providing a refund policy that states specific guidelines for the time period the customer has to return a product is critical.

What are the Challenges?

1. Friendly fraud is hard to detect.

Monitoring systems find friendly fraud hard to spot since it’s committed by legitimate customers doing legitimate transactions. Though sometimes the friendly fraud starts as a true claim, what the customer chooses to do ultimately determines the outcome.

In most instances ‘customers’ (real, or disguised fraudsters) are more intentional with their crime; they may claim they didn’t receive items that they did, or they might state that the item received didn’t match the online description, the service provided didn’t meet their expectations, or they don’t remember making the purchase. Each of these instances can be very hard to detect since reports of this nature are often legitimate.

2. Friendly fraud is hard to predict.

Because friendly fraud is usually committed by what appears to be legitimate customers, it’s extremely hard to predict when it will occur. Sometimes, the fraudster may only request a chargeback for a portion of their order, or they may be an ongoing customer who normally doesn’t dispute anything but then chooses to dispute a rare order. It may not even be something they were initially planning or intending to do, but the fraud occurs when they knowingly accept a refund for something they know they should be paying for.

3. Friendly fraudsters wait longer to initiate their chargebacks

The report by Fraud.net found that friendly fraud takes approximately 40% longer for a customer to report than third-party fraud. Third-party fraud is committed by someone who is not the cardholder or the merchant. Examples include identity theft and account hacking. So, a customer who notices a fraudulent charge on their account committed by a third party reports that fraud up to 11 days sooner than when attempting to commit first-party fraud. This time difference can affect the merchant’s anti-fraud attempts, return policies, accounting processes, and more.

4. Businesses are reluctant to flag friendly fraud.

Perhaps the biggest issue that online businesses face is a general unwillingness to mark these returns as fraud. Merchants using rules-based scores typically assign only 17% of the risk to a first-party fraud order as they assign to its third-party equivalent. Merchants blacklist first-party Fraudsters only 15% of the time compared to over 85% in third-party Fraud scenarios. This enables the first-party perpetrators to continue their schemes, often habitually. On average, the first-party fraudsters committed 9 instances of fraud, 3 times more than their third-party counterparts, and are likely still continuing their fraudulent behavior undeterred. Finally, for every chargeback received, merchants issue 7.5 refunds. We estimate that for every first-party Fraud chargeback, there are 2 refunds that are given directly to the fraudster, heading off the necessity for a chargeback. Therefore, the true out-of-pocket cost attributable to first-party fraud is 3 times the recorded cost of ‘friendly' fraud chargebacks.

How Do You Prevent Friendly Fraud?

Because their crimes are hard to recognize, successful friendly fraudsters are often habitual offenders. However, there are some methods you can put in place to minimize risk to your company.

- Participate in a consortium data partnership, where merchants and payment processors share anonymous data about bad actors in their systems.

- Establish a robust first-party fraud monitoring program that includes flagging repeat offenders.

- Incorporate deep learning models to detect the sometimes subtle patterns of first-party fraud

Learn More

- Download: 2020 Friendly Fraud Benchmarking Report

- Listen: Podcast: First-Party Fraud Lowers Profits by 25%

- Read: Top Three Ways to Prevent Friendly Fraud

- Speak with a Fraud Prevention Specialist